Types of Down Payment Assistance.

Down Payment assistance programs allow you to buy a home with no money down. There are two primary types of programs one is a state sponsored program like MSHDA the other is a program offered by your lending institution. Gold Star Financial offers a conventional product called Gold Star Advantage DPA and a FHA product called Gold Star Select DPA.

Which Down Payment Assistance program is right for you?

If you have excellent credit and solid income and job history you probably want to look at the Gold Star Advantage. This will be a conventional loan and will adhere to standard conventional guidelines. If you have less than perfect credit maybe a ding here or there or you are just getting started as a first time buyer then the Gold Star Select would be the best option for you. Below I will explain the primary differences.

Gold Star Select DPA Requirements:

- Standard FHA guidelines must be Approve/Eligible.

- Minimum Credit score of 600.

- Second mortgage in the amount of 3.5% of Appraised Value paired with first mortgage.

- Second Mortgage rate is 2% over first Mortgage note rate.

- Second Mortgage is a full 10 year amortization of principle and interest.

- Must be paid of on sale or refinance, lender will not re subordinate.

- Can also be used with up to 6% seller concessions.

Gold Star Advantage DPA requirements:

- Standard Conventional guidelines must be Approve/Eligible.

- Minimum credit score of 660.

- income subject 140% of AMI.

- second mortgage is 4% of Appraised Value paired with first mortgage.

- Second mortgage is the same as the first mortgage note rate.

- Second mortgage is an interest only payment.

- Must be paid of on sale or refinance, lender will not re subordinate.

- Can also be paired with up to 3% seller concessions.

The post Home Buyer tips and tricks “Down Payment Assistance” appeared first on Gold Star Mortgage Financial Group .

]]>

When buying a home Closing Costs should be one of the main things to consider so I wanted to put down a brief summary of items that you will need to save up for. This is just a general purpose example. If your buying a condo r a new build you can have additional cost so keep that in mind.

As a loan officer I like to break things down into four categories: Down payment, Mortgage closing, Escrow items and third party costs.

Down Payment- this is the percentage of the price that you are putting down on the home ie 5% down.

Mortgage Closing Cost- This includes any lender fee’s such as underwriting fee’s, processing fee’s, credit report, flood certification, or Broker fee these are all considered Origination fee’s and sometimes are all lumped together as such. Discount fee’s or points are fee’s that are included in purchasing a lower rate and are not origination fee’s.

Escrow Items- This includes the money you will need for taxes and insurance. On a home purchase you will always need insurance for 1 year in advance.

You will also need money to set up your escrow account for future payment of taxes. I will also include here any taxes that are currently due and any prorated taxes that are due to the seller at closing.

Quick tip here is to add up the tax amounts divide by 12 and then multiple by 13. That will likely cover what you need. You could also add 10% to the total and be in the ball park.

Third Party Cost- This includes any title or escrow company fee’s appraisal fee’s any anything else due in association with HOA or real estate company.

The post Home Buyer Tips and Tricks “Closing Costs” appeared first on Gold Star Mortgage Financial Group .

]]>

{kind=link}

The other day a Client asked me what was included in their payment? I replied everything. They asked again and I realized that although my Answer was correct they still didn’t know what I was talking about so here it is, the break down and a full explanation.

You might here a mortgage professional say PITI or PITIMI when talking about your monthly payment. This refers to your monthly payment meaning Principle, Interest, Taxes, and Insurance. Most loans however require some form of mortgage insurance so your payment will also include that.

Here is the break down:

Principle- The amount that goes toward paying your loan down.

Interest- This is the cost of borrowing the money.

Taxes- divide your annual tax amounts by 12 to get your monthly tax payment.

Insurance- This is your annual home owners or Hazard insurance divided by 12

PMI or MIP- This is insurance typically required with less than 20% down. Also required on all FHA loans.

The post Home Buyer Tips and Tricks “Your Monthly Payment” appeared first on Gold Star Mortgage Financial Group .

]]>

Payment history can have the largest impact on your credit scores. Making on time payments is the most important aspect of your score. Credit is King!

Your credit works on a what have you done for me lately basis. The most recent late payment counts against you the most. A late payment in the last month might cost you up to 100 points on an installment loan and 50 points on a revolving loan. As time goes by the amount goes down. So think about your last 6 months credit history then 12 then 24. After 2 years late payments don’t matter that much anymore as far as your score goes. So even the worst credit score can be greatly improved with in 12 to 24 months.

A late payment happens when your payment is made 30 days after the due date. so if your car payment is due April 15 and your payment doesn’t get maid until after May 15th that will be reported as a 30 day late. As long as your payment is made before the 30 day mark it will not be reported late.

Paying the bills on time can be the first thing to establishing a good credit history so set aside some time around the end of every month to make all you payments. My bank sends out payments in a couple days so I usually do mine on the 25 of every month.

The post Home Buyer Tips and Tricks “Credit Scores #2″ appeared first on Gold Star Mortgage Financial Group .

]]>

Credit Utilization.

Of the main area’s that determine your Credit scores Credit utilization is one of the most important. There are two types of debt, revolving i.e. credit cards and installment i.e. a home or car loan. The main focus here is your credit card debt. You need to know what your credit limits are and what your credit balances are to figure out your credit utilization. Credit utilization is the sum of your credit balances divided by your total limits. For example if you have a discover card with a 5k limit and a 4k balance, A Master Card with a 10k limit and a 5k balance then your total high balance is 15k and your balance owed is 9k. Your utilization in this scenario would be %60.

The Chicken or the Egg.

A good rule of thumb here is that less than %50 is good, %30 is better, %10 is best, and %1 is elite. The higher your balances are the harder its going to be to have a good credit score. The credit algorithm views high balances and minimum payments as “your in over your head.” If you make more than your minimum payments or pay them off every month The algorithm says “you need more credit.” The more willing creditors are to extend you credit the higher your score can go. It’s kind of a chicken or the egg type thing but the moral of the story is if you can keep your total balance around %1 your credit limits and credit scores will all go up.

The post Home Buyer Tips and Tricks “Credit Scores #1″ appeared first on Gold Star Mortgage Financial Group .

]]>

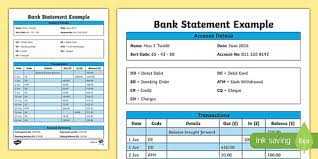

Bank Statements do’s and don’ts .

Bank statements are the number one pain point if you are buying a house. Your loan officer is going to ask for them over and over again and if you don’t provide the right stuff up front its going to be frustrating. Lets take a minute to understand exactly what an underwriter is looking for so we can make this as easy as possible.

Transaction Summery.

The minimum requirement for closing a loan is that you provide 60 days worth or 2 month’s bank statements dated with in 30 days of the closing date. This might mean that you will have to provide a transaction summary as well as 2 month’s bank statements. If you do, the first thing to know is that it has to have at least the last four digits of your account, your name and info, and your banks name as well as a URL from your bank. This is how all lenders verify your funds if your not using an electronic method. This is a standard practice and all banks provide this. Make sure there are no gaps. For example if your last statement date is on the first make sure your transaction summary includes that date.

Large Deposits.

What’s on these statements can be equally important and sometimes frustrating. Of course the first thing you need is enough money to cover the closing. After that your lender will be looking for things like large deposits, cash deposits and instances where your account has NSF charges (non sufficient funds).

Large deposits are typically defined by either an amount that exceeds 1% of your loan amount (typical for FHA loans) or 50% of your monthly income (conventional loans) depending on loan type. If this happens you will need to provide documentation for these deposits. Documenting with a copy of the check will generally suffice. Cash deposits generally are not allowed and will be backed out of your total. If your wondering why, It is part of the anti money laundering laws that lenders have to abide by.

The post Home Buyer Tips and Tricks “Bank Statements” appeared first on Gold Star Mortgage Financial Group .

]]>

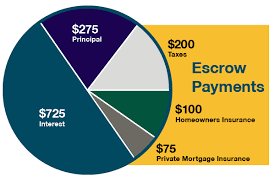

When is an Escrow account needed?

If you put less than 20% down you will be required to have an escrow account to pay your taxes and homeowners insurance. An escrow account is account your mortgage servicer will hold on your behalf to collect monthly amounts (included with your payment) to pay your taxes and insurance when they are due. Your lender does not collect interest on this account.

How does it work?

At closing your lender will collect payments to set up an escrow account. Generally they will collect monthly amounts in advance for summer tax, winter tax, school tax, and homeowners insurance. Which ever applies to your city \ county. For example: if your summer taxes are due in July and your first mortgage payment is due in March they will collect 7 month’s worth of that tax at closing. You would have made 5 payments by July therefore you would have 12 payments in escrow when this tax is due. Now there is enough to pay the total for the year.

What happens next?

Your servicer will also hold a reserve for overage at closing this will be called an aggregate adjustment on your closing disclosure. Generally a 2 month reserve for each item will be held. Each calendar year there after your account will be reviewed and a new reserve will be set up causing either a refund (if your taxes or insurance have gone down) or a shortage (if your taxes or insurance go up).

A shortage will require you to either mail in the short amount or increase your payment to cover the shortage over the next 12 month’s. This can feel like a double whammy in your payment because not only do you have to adjust for the increase you also have to make up the shortage. Sometimes it is better to just mail in the shortage amount to avoid drastic increases in your payment. This will typically happen after the first year you purchase a home. That is the time when your taxes can go up the most.

Its a good idea to review your annual escrow statement so you can anticipate your payment adjustment. One will be mailed to you every year on the anniversary of your closing.

The post Home Buyer tips and tricks “Your Escrow Account” appeared first on Gold Star Mortgage Financial Group .

]]>

Down Payment Sources.

When purchasing a new home one of the biggest items you need to understand is your down payment. There are many different types of mortgage products that offer down payments as low as zero to as much as you feel comfortable with. We will stick with the most common trends for the purpose of this article. Most people will fall into the 3% to 20% down payment range. Your down payment can come from the sale of your existing home, a savings, checking or investment account, a retirement account, a gift from a relative or a business account.What ever the case you need to provide proof of these funds typically for 60 days. If you don’t have proof of 60 days you will need to document where the funds came from.

A gift from a relative.

For example if its a gift from a relative you would need to provide a copy of the deposit into your account and usually an account statement from your donors account showing the transfer. Some times this will very slightly but go ahead and prepare yourself to provide this info to your lender. Also prepare the donor that they two might need to provide proof of their funs.

Self employed business funds.

If you are self employed and taking money from a business account for your down payment you will need to provide a letter from your CPA stating that you have 100% access to this money and it will not have negative impact on your business if you use it. This will also require that you provide 60 days of business statements.

Sale of existing property.

If your using money from the sale of an existing home you will just need to provide a settlement statement showing the proceeds from that sale. If the home has not sold yet but is under contract you can use a pre closing statement to show the funds and then an actual statement when you close.

Checking or savings account.

Now if you are just using a checking and or savings account to provide the down payment you need to make sure that the money is seasoned or you can prove where it came from. Cash deposits will not work in most cases so I would just rule it out.

Retirement accounts.

If you are using funds from a retirement account they need to be settled for example if you are withdrawing from a 401k or other account you will need to provide a copy of the check, the deposit and the terms of withdrawal from the account. This info is listed on every financial institutions web site. It might be hard to find but it is always there. If your down payment is in stocks or mutual funds you will need to sell those items and show the settled funds in your account.

Alternative methods.

If you had to sell a car or something like that you can provide the listing and bill of sale or something along those lines. Generally speaking you would need to provide some sort of proof you owned whatever item you are selling and a paper trail of the funds received. It would be better to get a check r something other than cash in this case.

Cash on hand.

If you are planning on purchasing a home and you are wanting to use “mattress money” it would be a good idea to go ahead and get that deposited into a bank account 60 days prior. Money that is seasoned or in an account for more than 60 days does not need to be verified and can save you some time and the frustration of having to provide extra documentation. Cash is not king when it comes time to put a down payment on a house so get it in the bank if that’s the case.

The post Home buyer tips and tricks the “down payment” appeared first on Gold Star Mortgage Financial Group .

]]>

Many clients inquire about bi-weekly payments. Bi-weekly payments are just as they sound, you make a payment every two weeks instead of every month. By doing this you can pay your loan off faster and you can line your payments up with your pay checks. By paying every 2 weeks you will make 26 payments a year. This is the same as making 13 monthly payments a year instead of 12. Most mortgage servicers allow you to do this if you request it. Once you have made your first monthly payment or your loan has been sold to your new servicer you can call customer support and set up bi-weekly payments. Most servicers will require that you do automatic withdrawals or ach payments as well. This makes the most sense to make sure you don’t forget to make a payment and all your payments are on time. An example of how much money you can save by making bi-weekly payments would go something like this. I’ll use a $200,000 mortgage at an interest rate of 4.75%.

The Monthly payment would be $1043.29 for Principle and Interest. The total interest paid would be $175,586.08 assuming you make your minimum payment every month. If you do bi weekly payment’s you would pay $521.65 every 2 weeks and your total interest would be $143,407.66. You can see that you can save $32,178.42 using biweekly payments. That is a considerable savings. In addition to the interest savings you will also pay your loan off in about 25 years instead of 30. I always recommend trying to do a shorter term if you ca swing it. Doing a 15 year loan instead of a 30 could save you the cost of college.

Another way to do this without making bi-weekly payments is just making an additional payment every year. This will effectively do the same thing. Any additional interest payments especially at the beginning of the loan term save you money. Just by paying an extra principle amount of $100.00 on your first payment will save you $313 over a thirty year term so you could see how that can add up over time!

The post Home Buyer Tips and Tricks “Bi-Weekly Payments” appeared first on Gold Star Mortgage Financial Group .

]]>